Who can apply for a co-borrowing house loan?

Last updated: 3 Sept 2025

1087 Views

Co-borrowing is one way to make your dream of owning your own home easier. This is because co-borrowing allows you to get approved for a home loan more easily than if you apply alone. This is because co-borrowing involves combining your income and repayment capacity with your co-borrower's, increasing the bank's chances of approving the loan.

However, co-borrowing doesn't mean you can just apply with anyone. Those you can ask to co-borrow from include:

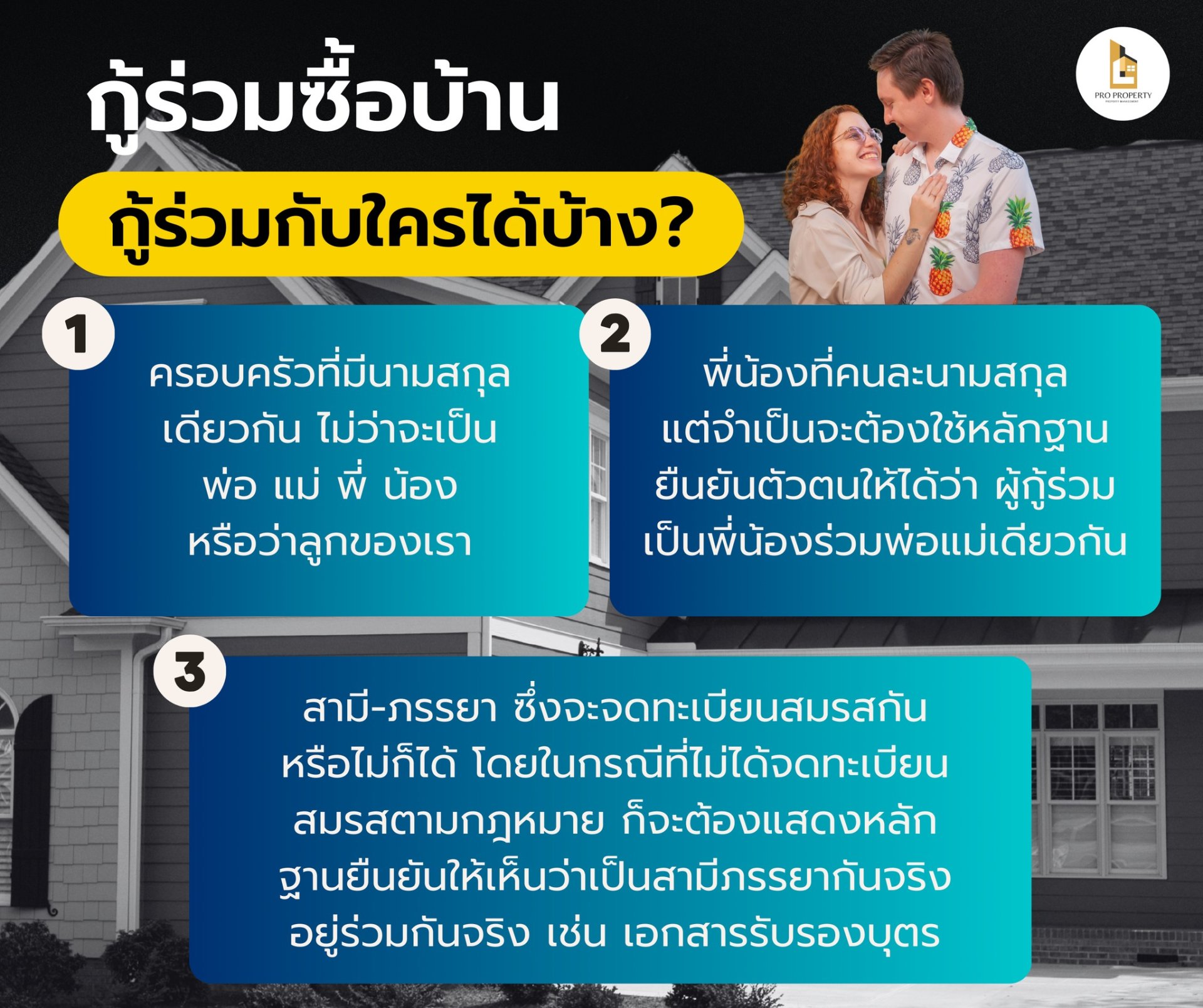

Family members with the same last name, whether it's your father, mother, siblings, or children.

Siblings with different last names are required to provide proof of identity that the co-borrower is your sibling.

Husband and wife, whether legally married or not. If they aren't legally married, proof of marriage, such as a child birth certificate, must be provided to prove that they are husband and wife and live together.

___________________________________________

Can LGBT couples apply for co-borrowing?

Equality and diversity are now widely accepted. This has led many LGBT couples to question whether they can jointly apply for a home loan. According to the principles of joint loans, joint loans are not possible because there is no evidence of legal relationship, such as parent, sibling, or husband and wife. However, the Marriage Equality Act is currently under review and is likely to be approved, providing equal rights to all. Therefore, many banks now allow LGBT couples to jointly apply for home loans, such as Bank of Ayudhya, Kasikornbank, etc. The conditions will be as specified by each bank.

___________________________________________

What are the special precautions to take into account when applying for a joint home loan?

Although joint loans are generally only available to family and legally-acquired partners to reduce the risk of conflict and disputes during the joint loan period, in reality, the long term of joint loans can always present challenges. Therefore, both co-borrowers must carefully consider the pros and cons to avoid further conflicts. Crucially, if any circumstances prevent them from making the required payments, the home could still be foreclosed. Therefore, joint loans are not simply about finding a way to get the loan approved. But it's also a matter of shared responsibility to make the loan payments until the final installment.

___________________________________________

Joint home loans can certainly make it easier to get approved. However, this means that the person you're bringing with you must have a stable income, be free of excessive debt, and be able to repay the loan. Otherwise, even a joint loan with two people may not be enough to get the bank to approve it. Furthermore, the price of the house or condo you're buying should not exceed your repayment capabilities. Finally, to ensure a smooth home loan and successful transfer of ownership, both the borrower and the co-borrower must maintain strict financial discipline.

___________________________________________

Source: REIC

However, co-borrowing doesn't mean you can just apply with anyone. Those you can ask to co-borrow from include:

Family members with the same last name, whether it's your father, mother, siblings, or children.

Siblings with different last names are required to provide proof of identity that the co-borrower is your sibling.

Husband and wife, whether legally married or not. If they aren't legally married, proof of marriage, such as a child birth certificate, must be provided to prove that they are husband and wife and live together.

___________________________________________

Can LGBT couples apply for co-borrowing?

Equality and diversity are now widely accepted. This has led many LGBT couples to question whether they can jointly apply for a home loan. According to the principles of joint loans, joint loans are not possible because there is no evidence of legal relationship, such as parent, sibling, or husband and wife. However, the Marriage Equality Act is currently under review and is likely to be approved, providing equal rights to all. Therefore, many banks now allow LGBT couples to jointly apply for home loans, such as Bank of Ayudhya, Kasikornbank, etc. The conditions will be as specified by each bank.

___________________________________________

What are the special precautions to take into account when applying for a joint home loan?

Although joint loans are generally only available to family and legally-acquired partners to reduce the risk of conflict and disputes during the joint loan period, in reality, the long term of joint loans can always present challenges. Therefore, both co-borrowers must carefully consider the pros and cons to avoid further conflicts. Crucially, if any circumstances prevent them from making the required payments, the home could still be foreclosed. Therefore, joint loans are not simply about finding a way to get the loan approved. But it's also a matter of shared responsibility to make the loan payments until the final installment.

___________________________________________

Joint home loans can certainly make it easier to get approved. However, this means that the person you're bringing with you must have a stable income, be free of excessive debt, and be able to repay the loan. Otherwise, even a joint loan with two people may not be enough to get the bank to approve it. Furthermore, the price of the house or condo you're buying should not exceed your repayment capabilities. Finally, to ensure a smooth home loan and successful transfer of ownership, both the borrower and the co-borrower must maintain strict financial discipline.

___________________________________________

Source: REIC

Related Content

25 Aug 2025

7 Mar 2026