Need to get a loan for another house. How can I get it approved?

This can change at any time. Initially, you were paying for a small house or a small condo alone. When you get married, have a family, have children, or have relatives move in, you may need to buy a larger house. Sometimes, you're paying for a house with your family, but then you have to move to a new workplace, which may necessitate you to purchase another condo closer to your office for easier commuting. When these situations arise, the question often arises: Can you afford a second house if you haven't finished paying off your first one? Will you be able to get a bank loan? The answer is yes, but you need to be financially prepared. Here are some guidelines to help increase your chances of getting a second house approved:

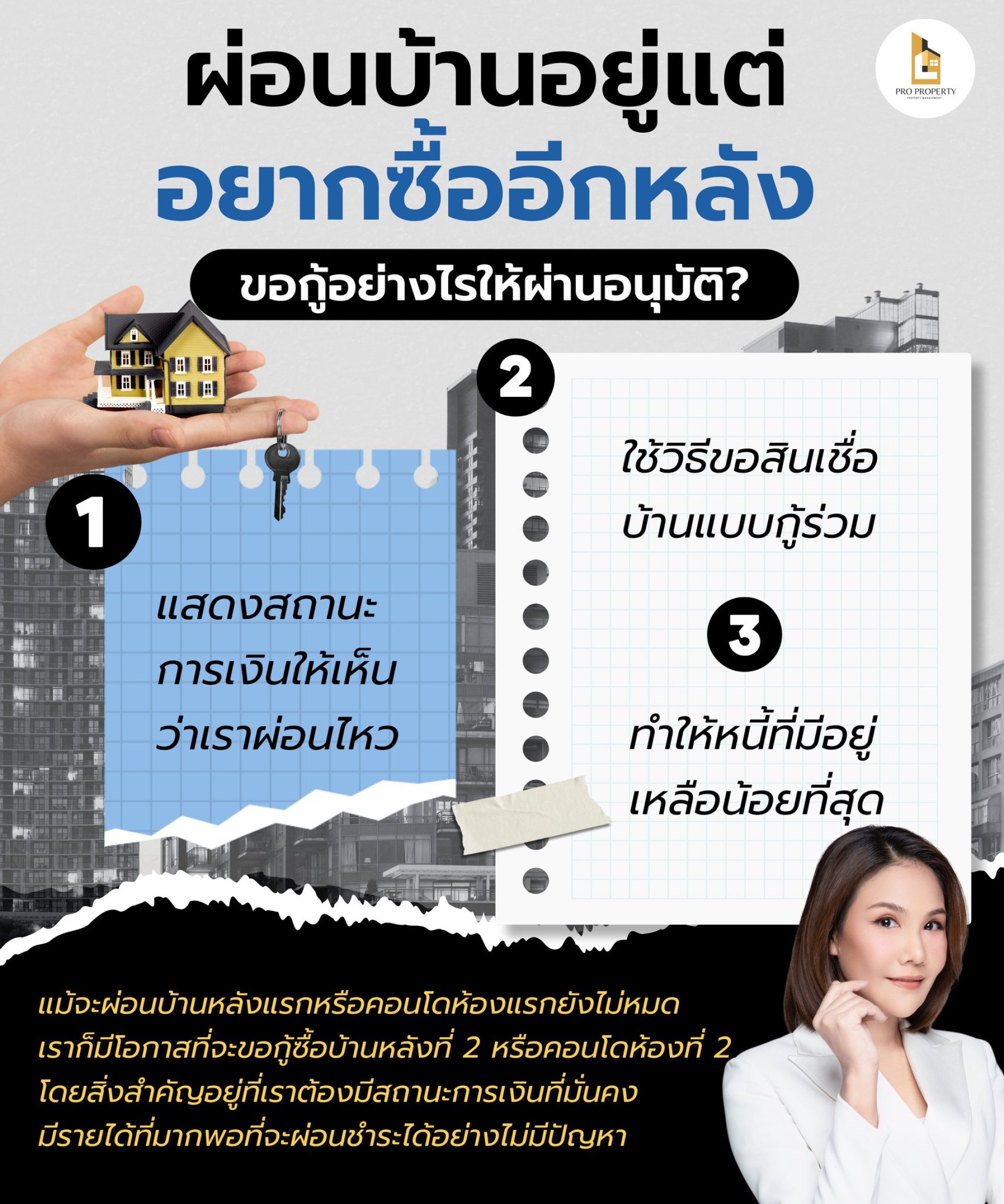

Demonstrate your financial ability to repay.

The most important principle in bank loan approval is that banks will only approve a loan after they have verified that you can afford the repayments. Therefore, borrowers must demonstrate their financial ability to repay. The method for calculating repayment ability is as follows: A person should not have a monthly mortgage payment exceeding 40% of their salary. For example, if their monthly salary is 100,000 baht, their monthly mortgage payment should not exceed 40,000 baht. Therefore, if your first house mortgage payment is 15,000 baht per month, you still have 25,000 baht remaining to pay. If you apply for a house loan with a monthly payment of no more than 25,000 baht, your chances of getting approved are relatively low. However, don't forget about your other debts, such as car payments or other loans. If you have significant debt and find that your repayment capacity is insufficient, you may also be denied a loan. Therefore, if you want to get a second house loan while still paying off your first house, you need to assess your repayment capacity to choose a second house at a price that's more suitable for your loan application. Alternatively, you can increase your income to increase your repayment capacity.

___________________________________________

Apply for a joint house loan.

The reason for the loan rejection is because the bank believes you can't afford the payments or your income isn't sufficient. This includes the debt on your first house, along with other debts that increase your risk. If you can't directly improve your ability to repay, you need to get someone with the ability to repay to join you. A joint loan is like combining two people's salaries. Combining their ability to repay improves your financial status significantly compared to a single loan, making it easier to get a second house loan approved. However, we also need to consider the financial status of the co-borrower. If the co-borrower's salary is low and they have a lot of debt, the combined loan may still be rejected.

___________________________________________

Minimize Existing Debt

The borrower's ability to repay can be increased if not by earning more income. By getting a co-borrower, you need to reduce existing debt. A lower monthly payment immediately increases your ability to repay. There are two main approaches to this: refinancing your first house to a lower interest rate and a lower payment amount, but this can only be done if you've been paying for it for three years. Another approach is to maximize the down payment on the second house. A larger down payment will reduce the loan amount, which means less debt. Or, the installment payments for the second house will be lower, making it easier for us to get approved by the bank.

___________________________________________

Even if we haven't finished paying off our first house or condo, we still have the opportunity to apply for a loan for a second house or condo from the bank. The key is to have a stable financial status and sufficient income to make the payments without any problems. However, even if we have a stable financial status and the ability to make the payments that the bank approves, we must also ensure that we have the financial discipline to effectively manage our expenses. Paying off two houses simultaneously is a heavy burden. Poor financial management or inadequate financial risk assessment, such as losing our job mid-term, can lead to insufficient cash flow and a financial crisis for our lives and loved ones.

___________________________________________

Source: REIC