3 things to check before buying a house

Last updated: 3 Aug 2025

1204 Views

A first home or condo is something we all desire and want to own as soon as possible. However, while it may seem like developers are offering numerous promotions, enticing us that buying a home or condo isn't difficult, the reality is that the expenses associated with owning a home are quite substantial. So today, to ensure that owning a first home is a positive experience that maximizes your happiness and prevents you from becoming burdened by debt and future misery, we'll take a look at a checklist of essential considerations before deciding to buy a home.

__________________________________________

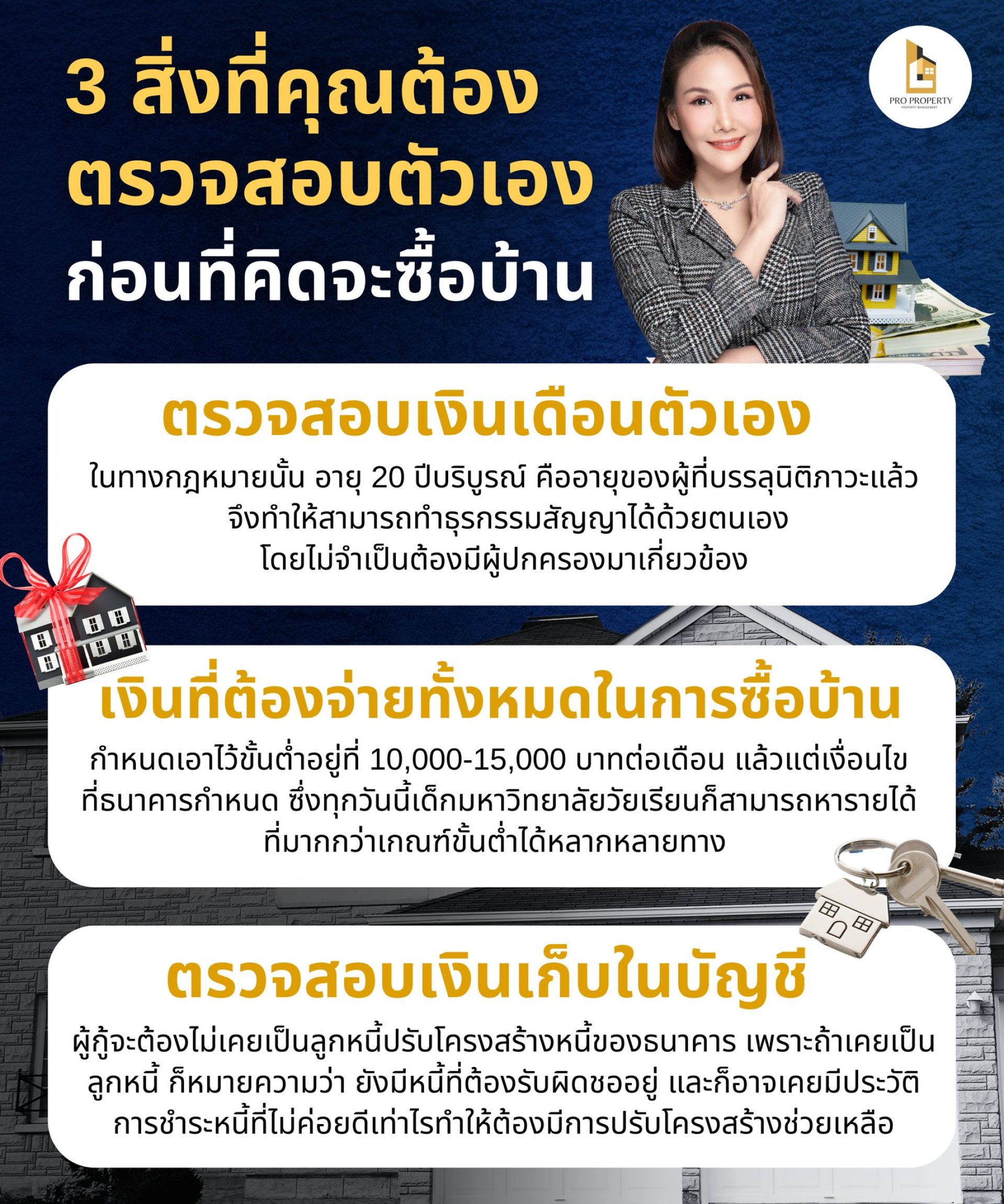

1. Check Your Salary

A question we're often asked is: How much salary do you need to buy a home? In reality, salary may not be the answer; you should also consider your debt-to-salary ratio. This is why homebuying advice is crucial. Our total monthly debt repayments should not exceed 40%. Simply put, if we earn 30,000 baht per month, our monthly debt repayments should not exceed 12,000 baht. Most people may assume that a 30,000 baht salary would allow us to comfortably purchase a house or condo with installments of no more than 12,000 baht per month. Therefore, when we see sales pitches that offer monthly payments in the thousands, it's easy to feel like we're ready to buy a home. However, in reality, 12,000 baht represents our total monthly debt repayments. This doesn't just include the house payment, but also includes other debts such as credit card debt, car loans, etc. If we don't include these debts, our monthly debt burden will be so high that we may not have enough money left over for living expenses or savings. In a bad economic climate, if our company closes or receives a salary cut, life can be extremely difficult.

__________________________________________

2. Check the total amount required to purchase a home

When buying a home or condo, many people focus solely on the monthly payment. In reality, this is not always the case. Monthly installment payments are only a portion of the total cost of buying a home. This is why it's important to thoroughly understand the costs involved before purchasing a house or condo. These costs can range from thousands to tens of thousands of baht.

The down payment is approximately 5-10% of the home's price. For example, a 2 million baht home would cost 100,000-200,000 baht.

The appraisal fee for loan applications is approximately 1,000 to 3,000 baht, depending on the bank's requirements.

The mortgage registration fee is 1% of the mortgage amount or approximately 1% of the loan amount.

The stamp duty is 0.50% of the purchase price.

The transfer fee is 2% of the appraised value by the Land Department.

The home insurance premium depends on the home's value.

The water and electricity meter fees are approximately 1,000 to tens of thousands of baht.

The common area fees are based on the unit's size or the land area.

The furniture, appliances, and home décor fees are approximately 10% of the home's value.

__________________________________________

3. Check your savings account

After reviewing the expenses beyond the mortgage payment, we'll immediately see that buying a house or condo is actually quite expensive. And of course, there are obligations, such as higher water and electricity bills due to the larger size of the house. Therefore, before applying for a home loan, it's important to check your savings account to ensure you have enough to cover major expenses such as the down payment, mortgage registration fees, common area fees, furniture, and decorations. Without this money, the purchase of a home will be more difficult. If it's too much, you'll have to use up all your savings. Having no emergency savings can be risky. After buying a home, you'll face monthly obligations to repay, as well as daily living expenses and medical expenses in case of illness. This will help you avoid excessive pressure.

__________________________________________

Buying a home involves many other expenses that you may not have considered. Beyond these, changing your residence or location can increase your travel and living expenses. Therefore, before buying a home, Therefore, it's essential to thoroughly examine your financial situation and ensure you have enough money to cover your home and living expenses. Don't just consider the monthly installments as advertised. If you're buying a home for living, it's a debt burden that will only increase your expenses. This is different from buying a house or condo for rent or investment, where you don't have to bear monthly expenses and are investing in a long-term return. However, even if you're buying a home for investment and renting out, you need to plan carefully and carefully calculate your opportunities, as there's always the risk of loss and crisis, given the current economic uncertainty in both Thailand and the global economy.

__________________________________________

Thank you for the great information from REIC.

__________________________________________

1. Check Your Salary

A question we're often asked is: How much salary do you need to buy a home? In reality, salary may not be the answer; you should also consider your debt-to-salary ratio. This is why homebuying advice is crucial. Our total monthly debt repayments should not exceed 40%. Simply put, if we earn 30,000 baht per month, our monthly debt repayments should not exceed 12,000 baht. Most people may assume that a 30,000 baht salary would allow us to comfortably purchase a house or condo with installments of no more than 12,000 baht per month. Therefore, when we see sales pitches that offer monthly payments in the thousands, it's easy to feel like we're ready to buy a home. However, in reality, 12,000 baht represents our total monthly debt repayments. This doesn't just include the house payment, but also includes other debts such as credit card debt, car loans, etc. If we don't include these debts, our monthly debt burden will be so high that we may not have enough money left over for living expenses or savings. In a bad economic climate, if our company closes or receives a salary cut, life can be extremely difficult.

__________________________________________

2. Check the total amount required to purchase a home

When buying a home or condo, many people focus solely on the monthly payment. In reality, this is not always the case. Monthly installment payments are only a portion of the total cost of buying a home. This is why it's important to thoroughly understand the costs involved before purchasing a house or condo. These costs can range from thousands to tens of thousands of baht.

The down payment is approximately 5-10% of the home's price. For example, a 2 million baht home would cost 100,000-200,000 baht.

The appraisal fee for loan applications is approximately 1,000 to 3,000 baht, depending on the bank's requirements.

The mortgage registration fee is 1% of the mortgage amount or approximately 1% of the loan amount.

The stamp duty is 0.50% of the purchase price.

The transfer fee is 2% of the appraised value by the Land Department.

The home insurance premium depends on the home's value.

The water and electricity meter fees are approximately 1,000 to tens of thousands of baht.

The common area fees are based on the unit's size or the land area.

The furniture, appliances, and home décor fees are approximately 10% of the home's value.

__________________________________________

3. Check your savings account

After reviewing the expenses beyond the mortgage payment, we'll immediately see that buying a house or condo is actually quite expensive. And of course, there are obligations, such as higher water and electricity bills due to the larger size of the house. Therefore, before applying for a home loan, it's important to check your savings account to ensure you have enough to cover major expenses such as the down payment, mortgage registration fees, common area fees, furniture, and decorations. Without this money, the purchase of a home will be more difficult. If it's too much, you'll have to use up all your savings. Having no emergency savings can be risky. After buying a home, you'll face monthly obligations to repay, as well as daily living expenses and medical expenses in case of illness. This will help you avoid excessive pressure.

__________________________________________

Buying a home involves many other expenses that you may not have considered. Beyond these, changing your residence or location can increase your travel and living expenses. Therefore, before buying a home, Therefore, it's essential to thoroughly examine your financial situation and ensure you have enough money to cover your home and living expenses. Don't just consider the monthly installments as advertised. If you're buying a home for living, it's a debt burden that will only increase your expenses. This is different from buying a house or condo for rent or investment, where you don't have to bear monthly expenses and are investing in a long-term return. However, even if you're buying a home for investment and renting out, you need to plan carefully and carefully calculate your opportunities, as there's always the risk of loss and crisis, given the current economic uncertainty in both Thailand and the global economy.

__________________________________________

Thank you for the great information from REIC.

Related Content

16 Jul 2025

16 Jan 2026